Platform for investors

Find investment opportunities with context

Review projects, read market analysis, and check risk signals in one place before reaching out or committing capital.

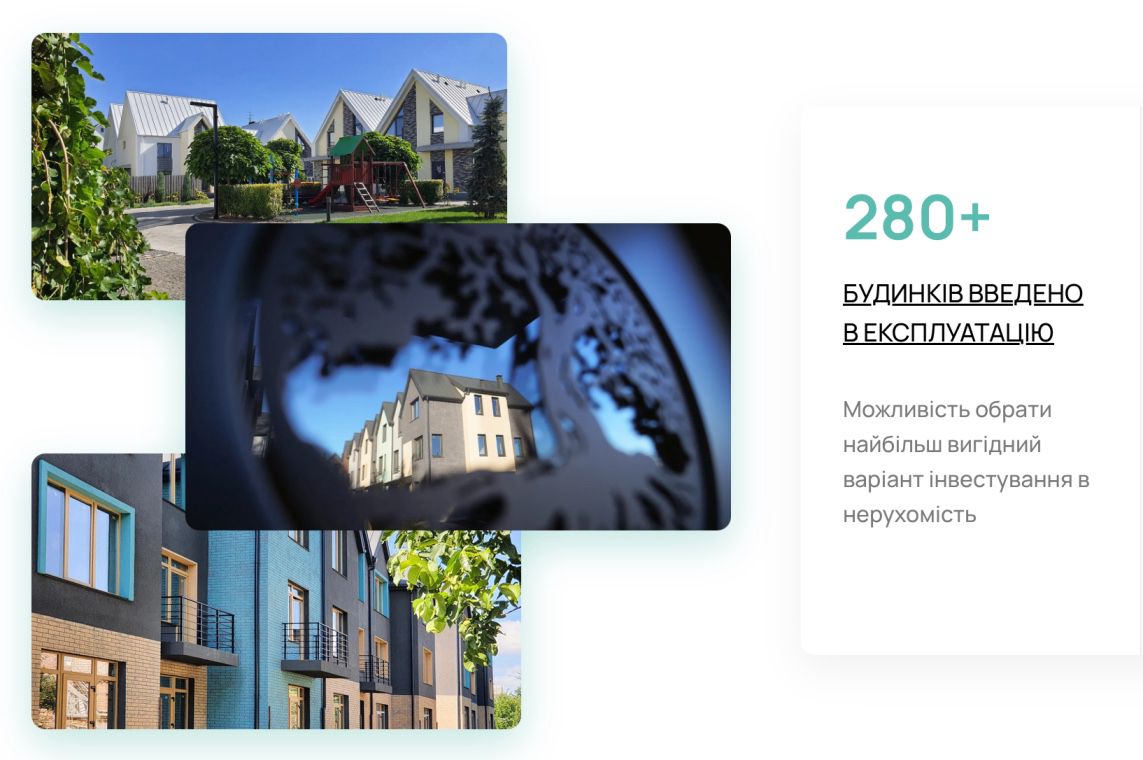

152

active opportunities

136

research pieces

9

risk flags and cases

Opportunities

Filter listings by sector.

Market context

Read reviews before reaching out.

Risk checks

Screen the blacklist before any negotiation.

For founders

Add your project to the radar for investor visibility.

Telegram updates

Subscribe to our Telegram channel

Get notifications about new projects, market news, and Invest Radar updates on Telegram.

Invest Radar

Compact signals without extra noise

Investment projects

Review opportunities by sector, entry terms, and the supporting material around them.

152Active

All projectsFilters apply across projects, news, and blacklist entries together so each topic keeps its context.

Market context

All coverageReviews and news

Use research as a second validation layer before making an investment decision.

Review and newsStartupOther

🚀 Venture Investing for Ukrainian Investors How the startup market works, where large returns are created, what risks investors must accept, and how to begin

🧭 What this article covers Venture investing means investing in young technology companies that have the potential to grow very quickly. It is not the same as: 🏦 placing money in a bank deposit; 📜 buying bonds; 📊 investing in public stocks; 🏪 investing in a traditional small business; 💳 lending money to an entrepreneur. Venture capital is a separate asset class characterized by: ⚠️ very high risk; ⏳ a long investment horizon; 🔒 low liquidity; 📉 a high startup failure rate; 🚀 potentially very large returns. A venture investor normally does not earn money from dividends. The investor earns when the startup reaches an exit : it is acquired by another company, goes public through an IPO, or its shares are sold to another investor in a secondary transaction. The central idea is simple: 💡 A venture investor invests not in the company’s current profit, but in its potential future growth. This is why venture investing is generally unsuitable for people who need guaranteed income, quick access to their money, or a low level of risk. 1. 💰 The three main objectives of investing Investors generally allocate their money for one of three broad reasons. 🛡️ 1. Preserving capital This is the most conservative objective. The primary purpose is not to generate an exceptionally high return, but to protect money from loss. Typical instruments may include: 🏦 deposits in reliable banks; 🥇 gold; 📜 government bonds issued by highly rated countries; 💵 other relatively low-risk financial instruments. These instruments are generally used for money that must be preserved rather than exposed to substantial risk. 📈 2. Growing capital Here, the investor accepts a higher level of risk in exchange for potentially higher returns. Typical instruments may include: 📊 public equities; 🏢 corporate bonds; 🌍 investments in developed and emerging markets; 🏗️ ownership stakes in operating businesses; 💳 business lending. The risk is higher than in capital-preservation instruments, but the potential return is also greater. 🚀 3. Building substantial wealth This category involves high-risk instruments with significant potential upside. Examples include: 🚀 venture capital; 🧪 direct startup investments; ₿ cryptoassets; 📉 speculative trading strategies; 💱 Forex and other leveraged markets. Venture capital belongs primarily to this third category. It is not designed to preserve capital. It is designed to give an investor exposure to companies that could potentially increase dramatically in value. 2. 🧠 What is venture investing? Venture investing is the financing of startups—young companies that usually: 💻 are built around technology; 🌍 can scale across large or international markets; 📈 aim to grow rapidly; 🔥 may not yet be profitable; 💸 require additional capital to continue growing; 🎯 could potentially become very large businesses. The venture investor provides capital with the expectation that the company will become more valuable over time. Unlike a bondholder, the investor does not receive a predetermined coupon. Unlike a bank depositor, the investor does not receive a guaranteed interest rate. Unlike an owner of a mature dividend-paying company, the venture investor usually receives no regular distributions. The expected return comes from the future sale of the investor’s ownership interest or contractual right to receive equity. 📌 The key difference A traditional business investor often asks: How much profit does this business generate today? A venture investor asks: How large could this company become in the future? The venture investor evaluates whether the company could potentially grow: 🚀 10 times; 🚀 50 times; 🚀 100 times; 🚀 or, in exceptional cases, 1,000 times. These large potential multiples make venture capital attractive. However: ⚠️ The possibility of earning 100x exists precisely because the probability of losing the investment is also very high. 3. 🏪 A startup is not the same as a small business One of the most common mistakes made by new investors is treating a startup and a small or medium-sized business as the same type of investment. They operate according to very different economic models. 🏪 A traditional small or medium-sized business Examples include: ☕ a coffee shop; 🍽️ a restaurant; 🛒 a retail store; 🚚 a logistics company; 🏭 a small manufacturing operation; 🧰 a local service business. Such a company is normally created to generate sustainable profit. An investor may expect: 💵 dividends; 📊 a share of operating profit; 💳 repayment of a loan with interest; 🏢 an increase in the value of the business. The business may be stable, profitable, and attractive. However, its growth may be limited by geography, operating capacity, margins, management resources, or the total size of its market. 🚀 A startup A classic definition associated with startup methodology describes a startup as a temporary organization searching for a repeatable and scalable business model. Once that model has been found and the company becomes an established, scalable operation, it gradually stops being a startup in the strictest sense. In modern market language, however, the term “startup” is often used more broadly for a technology company that: 💻 has a technology-based product; 💰 has raised venture capital; 📈 is pursuing rapid growth; 🏛️ has not yet completed an IPO. A startup can operate without profit for many years. This is not always a sign of failure. In venture-backed companies, cash is frequently reinvested into: 🧪 product development; 👨💻 engineering; 📣 marketing; 🧑💼 sales; 🔬 research and development; 🌍 geographic expansion; 🏗️ operational infrastructure; 🏁 capturing market share. 🔥 The fundamental distinction A traditional small business is expected to generate profit. A venture-backed startup is expected to grow very quickly. A small business may be a good investment if it is stable and profitable. A startup may be a good venture investment if it has a credible opportunity to become a very large technology company. 4. 🦄 What is a unicorn? A privately held startup with a valuation exceeding: 💰 $1 billion is commonly called a unicorn . This term matters because a small number of unicorns can generate a large proportion of the returns in a venture portfolio. An investor who entered a company at a valuation of $10 million or $20 million and retained exposure until the company exceeded a $1 billion valuation could potentially achieve a substantial increase in the paper value of the investment. However, valuation growth is not the same as realized cash. The investor only realizes a return when a liquidity event allows the shares to be sold. 📊 A figure mentioned in the talk The combined valuation of global unicorn companies was described during the talk as approximately: 🦄 $8.6 trillion The speakers emphasized that this value was created by young technology businesses built by entrepreneurs, engineers, researchers, students, and startup teams. This figure should be understood as a market estimate discussed during the presentation, not as a guaranteed or independently audited amount. 5. 🌍 Where are the strongest startup ecosystems? Startups exist in almost every country. However, not every country has an ecosystem that allows a startup to grow rapidly into a global company. A developed startup ecosystem requires more than talented founders. It usually includes: 🎓 strong universities; 👨💻 skilled engineers; 💰 angel investors and venture funds; 🚀 accelerators; ⚖️ experienced startup lawyers; 🏢 corporate buyers; 📈 accessible capital markets; 🌍 international customers; 🧠 experienced founders and operators; 🤝 networks that connect all market participants. For a venture investor, the strength of the ecosystem can be almost as important as the quality of the individual company. 📊 Geographic distribution discussed during the talk The presentation described the approximate distribution of unicorn companies as follows: 🇺🇸 United States — approximately 50% ; 🇨🇳 China — approximately 20% ; 🇮🇳 India — approximately 5% ; 🇬🇧 United Kingdom — approximately 5% . Together, these four countries were said to account for approximately: 🌍 80% of the world’s unicorn companies This concentration is highly relevant for investors. An investor seeking access to the strongest startups should evaluate not only the quality of an idea, but also whether the company is positioned inside an ecosystem capable of supporting global expansion. 🇺🇸 Why the United States is considered the leading venture market The United States, and Silicon Valley in particular, remains one of the principal global centers of venture capital. Its advantages include: 🎓 major research universities; 👨💻 a deep technology talent pool; 💰 many venture capital firms; 🧑💼 experienced angel investors; 🚀 established accelerators; 🏢 large technology corporations; ⚖️ a developed legal infrastructure; 📈 a culture that accepts entrepreneurial risk; 🌍 access to a large domestic and global market. The central conclusion expressed during the talk was that investors seeking access to top-tier startups need to find a practical route into the American venture ecosystem. ⚠️ Why all large markets are not equally accessible China has created many large technology companies, but foreign investors may face additional political, regulatory, ownership, and capital-repatriation risks. India has a very large internal market and produces important technology companies, but it also has its own regulatory, operating, and market-specific complexities. Europe has strong founders and companies, but the speakers argued that even major economies such as Germany, France, and Spain have not historically produced unicorns at the same rate as the United States. These statements reflect the speakers’ investment perspective and should not be treated as a universal rule. Excellent companies can emerge in any jurisdiction. 6. 📈 Why many of the largest returns are created before an IPO Historically, venture investors financed a startup until it reached a public-market stage. The company then completed an IPO, and public-market investors could participate in a substantial part of its later growth. Today, many successful technology companies remain private for longer. Large private funding rounds allow companies to raise significant capital without entering the stock market. As a result, a greater portion of value creation may occur while the company is still privately held. 📌 What this means for investors Public-market investors can still achieve substantial returns, including: 📈 2x; 📈 3x; 📈 5x; 📈 and sometimes 10x. However, the exceptional outcomes of: 🚀 50x; 🚀 100x; 🚀 or 1,000x are more likely to originate from investments made at the earliest stages of a successful technology company. The trade-off is straightforward: ⚠️ The earlier the investment, the larger the potential return—and the greater the probability of complete loss. 7. 🧺 Why venture investors need a portfolio Venture capital should not normally be approached as a single isolated bet. In business lending, an investor may expect every performing loan to produce interest. In real estate, each property may generate rental income. In a bond portfolio, each performing security may generate coupon payments or repayment at maturity. Venture portfolios behave differently. 🎯 The basic venture portfolio model Some startups will fail completely. Some may survive but produce no meaningful return. Some may return approximately the original capital. A smaller number may produce good returns. One or two exceptional companies may generate most of the value of the entire portfolio. This is often described as a power-law distribution : a very small number of investments create a disproportionately large share of total returns. 📊 Portfolio example from the talk The speakers referred to a portfolio containing approximately: 🧺 110 startups Several companies were described as having generated or indicated large multiples, including approximately: 🚀 30x; 🚀 50x. Many of the remaining companies were still developing, and their final outcomes were not yet known. This demonstrates the logic of venture diversification: every company does not need to succeed, but the portfolio needs enough exposure to potential outliers. 8. ⚰️ Startup mortality: expected, but financially painful Startup failure is not an unusual exception. It is a structural characteristic of the venture market. 📊 Statistics discussed during the talk The speakers gave an illustrative example: Out of 1,000 startups , approximately 10 might eventually become unicorns. That would represent roughly 1% of the original group. The talk also mentioned a model connecting failure probability with the amount of capital already raised: 📉 for a very early startup with little validated financing, the probability of failure was described as approximately 55% ; 📉 if approximately $2 million had already been invested, the probability of failure was described as falling to approximately 14% . These figures should be treated as indicative statistics from the talk rather than universal probabilities applicable to every company, sector, or stage. Capital raised may be a useful signal, but it does not prove that a startup is healthy. A well-funded company can still fail. 💸 Why startups fail The primary cause highlighted during the presentation was: 💸 Running out of cash Startups frequently operate at a loss because they spend heavily on: 👨💻 employees; 🧪 product development; 📣 marketing; 🧑💼 sales; ⚙️ infrastructure; 🌍 expansion. If a startup does not reach the required milestones before its cash runs out, and it cannot raise another financing round, the company may be forced to close. ⚠️ Other common reasons for startup failure ❌ The target market is smaller than expected. ❌ The product does not solve an important enough problem. ❌ Customers are unwilling to pay. ❌ The founding team cannot execute. ❌ Competitors move faster. ❌ Unit economics do not work. ❌ Sales cannot be scaled efficiently. ❌ The technology does not perform as expected. ❌ Founders enter into serious conflict. ❌ Regulation changes the commercial opportunity. ❌ The company cannot raise its next round. A venture investor must be psychologically and financially prepared for losses within the portfolio. 9. 🧬 Why technology is central to venture capital The talk suggested that approximately: 💻 90% of startups are technology businesses Technology matters because it can give a startup a temporary competitive advantage. If a business model is easy to copy, competitors can enter quickly and reduce margins. A company may have stronger protection if it possesses: 🧠 proprietary artificial intelligence; 📊 unique data; 🧮 algorithms; 🔩 specialized hardware; 💻 complex software; 👁️ computer-vision capabilities; 📜 patents or intellectual property; 🌐 network effects; 🏗️ difficult-to-replicate infrastructure; 👨🔬 a uniquely qualified technical team. Technology does not guarantee success. However, it may give the startup enough time to build distribution, win customers, improve the product, and establish a defensible market position. ⏳ Technology becomes obsolete quickly A capability that was innovative 10 or 15 years ago may now be a commodity. The talk used e-commerce as an example. Building an online store was once a technically difficult and highly innovative project. Today, a basic e-commerce operation can be launched using ready-made platforms and automated tools. This is why venture investors continually search for new technology cycles rather than investing only in technologies that were disruptive in the past. 10. 🪜 Stages of venture financing A startup does not normally raise all the capital it needs at once. It progresses through several financing stages. At each stage, the following may change: 💰 the amount raised; 🏷️ the company’s valuation; ⚠️ the investment risk; 👥 the types of investors involved; 📈 the operating milestones expected by investors. 🌱 Pre-seed Pre-seed is usually the earliest institutional or semi-institutional financing stage. The company may have only: 💡 an idea; 🧪 a prototype; 👥 a small founding team; 📄 a pitch deck; 🔍 early customer research; 📦 an initial minimum viable product. Investors at this stage may include: 👨👩👧👦 friends and family; 😅 so-called “friends, family, and fools”; 🧑💼 angel investors; 🚀 accelerators. 📊 Figure mentioned in the talk The speakers stated that a pre-seed company in Silicon Valley might raise up to approximately: 💰 $500,000 They also emphasized that many investors no longer want to finance only an idea. Founders are increasingly expected to build an initial product, attract first users, or generate early sales before approaching professional investors. 🌾 Seed At the seed stage, the startup should normally have more than a concept. It may already have: 📦 a functioning product; 👥 initial users; 💳 early customers; 📈 evidence of demand; 🔁 early retention data; 🧪 pilot projects. At this stage, the company is trying to demonstrate that its product can become a scalable business. 📊 Seed-stage figures mentioned during the talk The presentation gave an indicative seed-stage valuation of approximately: 🏷️ Up to $20 million The average seed raise was described as approximately: 💰 $3.5 million Examples of seed-round sizes included: 💰 $1.5 million; 💰 $3.5 million; 💰 $5 million. The actual size of a seed round depends on the sector, country, team, traction, market conditions, and investor demand. 🅰️ Series A Series A is a more mature institutional financing stage. Investors normally expect evidence such as: 📈 meaningful traction; 💰 revenue; 👥 paying customers; 🔁 customer retention; 📊 measurable growth; 🧩 a credible business model; 🌍 a sufficiently large market; 🏗️ a plan for scaling the organization. At this stage, investors rely less on the founders’ vision alone and more on operating data. 📊 Series A figure mentioned during the talk The presentation gave an indicative average Series A raise of approximately: 💰 $15 million This should be understood as a market reference point, not a fixed rule. Some companies raise substantially less, while highly competitive companies in capital-intensive sectors may raise much more. 🅱️ Series B, Series C, and later rounds At later stages, the company is expected to have: 💰 significant revenue; 👥 an established team; 🌍 a proven market; 📈 rapid growth; 🏗️ more mature operations; 📊 more reliable performance data. The risk may be lower than at pre-seed or seed, but the company’s valuation is usually much higher. Therefore, the potential investment multiple is generally lower. Later-stage investors may include: 🏦 large venture funds; 📈 growth-equity funds; 🏛️ private-equity investors; 🏢 strategic corporate investors; 💼 institutional secondary investors. 11. 👥 Participants in the venture market The venture ecosystem contains several categories of investors and support organizations. 👨👩👧 Friends, family, and fools These are often the first external people to finance a founder. Their investment may be based primarily on personal trust rather than a professional assessment of the business. The phrase “friends, family, and fools” is informal industry language. It reflects the extremely high risk of investing before meaningful evidence has been created. 🧑💼 Angel investors Angel investors are private individuals who invest their own money into early-stage companies. In addition to capital, a strong angel may provide: 🤝 business connections; 🧠 operating experience; 🚪 access to customers; 👨💻 help with recruitment; 📣 reputational support; 💰 introductions to later investors. The speakers argued that traditional angel groups have become less dominant in Silicon Valley than they were previously, partly because accelerators, seed funds, and syndicates now perform many of the same functions. 🚀 Accelerators Accelerators select early-stage companies and help them develop quickly. They may provide: 💰 initial capital; 🧠 mentoring; 📚 education; 🤝 access to a founder network; 🎤 a demo day; 🚪 introductions to venture investors. 📊 Accelerator example from the talk Y Combinator was mentioned as one of the best-known startup accelerators. The investment associated with its early-stage program was described as approximately: 💰 $500,000 The speakers also mentioned emerging competitors and specialized accelerator programs, including programs serving Ukrainian defense-technology startups. 🌱 Seed funds Seed funds specialize in financing early-stage companies that may already have a product, initial sales, or early market validation. Their teams usually evaluate many opportunities and create diversified portfolios of young companies. 🏦 Venture capital funds Venture capital funds collect capital from investors known as limited partners , or LPs. The fund’s management team then: 🔍 identifies startups; 📊 performs due diligence; ⚖️ negotiates investment terms; 🧺 builds a portfolio; 🤝 supports portfolio companies; 🚪 manages exits. The speakers referred to venture-fund investment checks of: 💰 $5 million; 💰 $10 million; 💰 $20 million; 💰 and, in some cases, $100 million. Actual check sizes differ significantly depending on the fund’s strategy and the startup’s stage. 🏛️ Private-equity and growth funds Private-equity and growth investors normally participate at later stages. They may invest hundreds of millions or, in very large transactions, billions of dollars. These investors generally seek more mature companies with significant revenue, stronger governance, and a clearer path to liquidity. 🏢 Corporations Corporations may participate in the startup market by: buying startups through acquisitions; investing through corporate venture capital funds; acquiring access to technology or intellectual property; recruiting specialized teams; entering new markets; preventing competitors from gaining strategic assets. A corporation may therefore invest for strategic reasons rather than purely for financial return. 12. 📄 SAFE and convertible notes At an early stage, an investor does not always receive shares immediately. Instead, the investment may be structured through an instrument that converts into equity during a later financing round. The two most common instruments discussed were: 📄 SAFE agreements; 📄 convertible notes. 📄 SAFE SAFE stands for Simple Agreement for Future Equity . In simplified terms: The investor provides capital now, but the exact number of shares is determined later, usually when the startup completes a future priced equity round. A SAFE is generally not the same as a traditional loan. It normally has no standard repayment schedule or regular interest obligation, although the precise terms depend on the document and jurisdiction. 📄 Convertible note A convertible note is a debt instrument that may convert into equity during a later financing event. Unlike a SAFE, it may include: 📅 a maturity date; 💵 interest; 🔄 conversion provisions; ⚖️ repayment or restructuring consequences. 📊 Market shift mentioned during the talk The speakers stated that earlier in the market: convertible notes represented approximately 90% of early-stage instruments, while SAFEs represented approximately 10% . They argued that the relationship has now largely reversed, with SAFEs becoming much more common in Silicon Valley’s early-stage market. The precise market share changes over time and differs by jurisdiction, so these percentages should be viewed as an illustration of the trend. 🔍 Important SAFE and convertible-note terms An investor must understand at least the following: 🏷️ Valuation cap The valuation cap establishes the maximum company valuation used to calculate the investor’s conversion price. A lower cap is generally more favorable to the early investor, because it may result in more shares upon conversion. 💸 Discount The discount allows the early investor to convert at a lower price than the price paid by investors in the next financing round. For example, a 20% discount may allow the SAFE holder to convert at 80% of the new investor’s price, subject to the document’s terms. 🔄 Conversion mechanics The agreement should explain: what event triggers conversion; which class of shares the investor receives; how the conversion price is calculated; what happens during an acquisition or shutdown; whether the cap or discount applies. 📉 Dilution Dilution occurs when the company issues additional shares. The investor may still own the same number of shares, but those shares represent a smaller percentage of the company. 📌 Pro rata rights Pro rata rights may allow the investor to participate in future rounds in order to maintain its percentage ownership. 📄 Information rights Information rights determine what financial, operational, and governance information the investor can receive. ⚖️ Liquidation preferences In priced equity rounds, preferred shareholders may receive priority over common shareholders when proceeds are distributed during a sale or liquidation. Two investments of the same monetary amount can produce very different economic outcomes because of differences in these terms. 13. 💵 How a venture investor earns a return Startups almost never pay dividends. The speakers stated that throughout their experience they had rarely, if ever, seen venture-backed startups pay dividends to early investors. This is logical: a high-growth startup normally reinvests available capital into expansion rather than distributing it. The investor therefore depends on an exit. 🚪 Main types of venture exits 1. 🏢 M&A M&A means mergers and acquisitions . In the most common scenario, a larger company acquires the startup. The buyer may be interested in: 💻 the product; 🧠 the technology; 👥 the team; 📊 the customer base; 📜 intellectual property; 🌍 access to a new market; 🏁 eliminating or absorbing a competitor. 📊 M&A figure mentioned in the talk The speakers estimated that approximately: 🏢 90% of startup exits occur through M&A This was presented as a broad practical estimate rather than a precise universal statistic. 2. 🏛️ IPO An IPO, or initial public offering, is the process through which a private company lists shares on a public stock exchange. An IPO can create liquidity for investors, but early shareholders are often subject to: 🔒 lock-up periods; 📄 trading restrictions; 📉 market-price volatility; ⚖️ securities-law requirements. 📊 IPO figure mentioned in the talk The speakers estimated that approximately: 🏛️ 10% of startup exits occur through IPOs The intended message was that IPOs attract significant attention but are much less common than acquisitions. 3. 🔁 Secondary sale A secondary transaction occurs when an existing shareholder sells shares to another investor before the company completes an IPO or acquisition. For example, a new Series B investor may offer to purchase some shares from earlier investors. A secondary sale can allow an early investor to: 💵 realize part of the return; ⚖️ reduce portfolio risk; 📈 retain part of the position for further upside; 🔄 return capital to investors before the final company exit. Secondary transactions may be restricted by company approval requirements, rights of first refusal, securities laws, shareholder agreements, or transfer limitations. 14. 🔒 Liquidity: why venture capital is not the stock market A public-market investor can usually sell listed shares during market hours. A private-company investor cannot simply press a “sell” button. Private shares may be subject to: 🔒 lock-up restrictions; 📄 company approval; ⚖️ shareholder-agreement provisions; 👤 a limited number of qualified buyers; 📉 discounts for illiquidity; 🧾 limited publicly available information; 🚫 rights of first refusal; 🏛️ regulatory requirements. Even if a startup’s valuation has increased, the investor may be unable to convert that paper gain into cash. 📊 Discount example discussed during the talk The speakers described an example involving restricted private-company shares purchased at a discount of approximately: 💸 70% The discount was associated with lock-up restrictions, transfer limitations, and the uncertainty surrounding illiquid shares. Such a discount is not automatically a bargain. A large discount may reflect: ⚠️ legal restrictions; ⚠️ limited transferability; ⚠️ uncertain liquidity; ⚠️ information asymmetry; ⚠️ the possibility that the stated valuation is not realizable. 15. 📊 How to evaluate a startup Professional venture investors may use dozens of criteria. The speakers stated that their team uses approximately: 🔍 40 criteria The weighting of those criteria changes depending on the company’s stage. At pre-seed and seed, the team may be the dominant factor. At Series A and later, revenue, growth, retention, unit economics, and execution data become increasingly important. 👥 1. The founding team At the earliest stage, the team may be more important than the current product. Investors should evaluate: Does the team have relevant experience? Do the founders understand the customer and market? Can they recruit strong employees? Can they sell? Can they raise future financing? Can they learn quickly? Can they survive prolonged stress? Can they change direction when the original idea fails? Do the founders trust one another? Are incentives and ownership structured appropriately? A weak team can destroy a strong idea. A strong team may change the product, revise the business model, and still build a successful company. 📈 2. Traction Traction is evidence that the company is moving in the right direction. It may include: 💰 revenue; 👥 active users; 📄 signed contracts; 🔁 retention; 📊 growth rate; 🧪 successful pilots; 🤝 partnerships; 📣 organic referrals; 🛒 repeat purchases. The relevant traction metric depends on the business model. For a B2B software company, annual recurring revenue may matter. For a consumer platform, active users and retention may matter more. For Defense Tech or industrial hardware, paid pilots, field testing, procurement contracts, and production capacity may be central. 💰 3. Revenue Revenue is one of the strongest forms of validation. The speakers stated that, for some syndicated investments, they typically looked for companies with more than approximately: 💰 $1 million in revenue Alternatively, they might invest when another trusted professional venture fund was participating in the round. Revenue should never be assessed in isolation. Investors should ask: Is the revenue recurring? How concentrated is it among customers? What is the gross margin? How quickly is it growing? What is customer churn? How much does it cost to acquire a customer? How long does the sales cycle take? Can the company scale without spending proportionally more? 📊 4. Growth rate The talk referred to a strong growth benchmark of approximately: 📈 3x annual revenue growth In startup language, this generally means tripling revenue over one year, not growing by 3%. The distinction is critical: A 3% annual growth rate would be relatively modest for an early venture-backed startup. A 3x annual growth rate means revenue becomes three times larger. The transcript appears to contain some ambiguity in this part, but the surrounding context indicates that the intended meaning was likely approximately threefold annual growth. 🌍 5. Market size A venture-backed company needs a sufficiently large market. A good product in a very small market may become a profitable business but may never become large enough to generate venture-scale returns. Investors should ask: How large is the total addressable market? Is the market growing? Is the customer problem urgent? Who controls the purchasing budget? Are customers willing to pay now? Can the company expand internationally? Is the market constrained by regulation or procurement? Can the startup become a category leader? 🧬 6. Technological defensibility The investor should understand why competitors cannot immediately copy the product. Potential sources of defensibility include: 🧠 proprietary AI; 📊 unique datasets; 🧮 specialized algorithms; 🔩 difficult hardware engineering; 💻 deeply integrated software; 👁️ computer vision; 📜 patents; 🌐 network effects; 🏗️ complex infrastructure; 🤝 exclusive partnerships; 🚪 privileged distribution. Technology alone is not enough. A technically advanced product without customers may still be a poor investment. ⚖️ 7. Deal terms A strong startup may still be a poor investment if the entry valuation is excessive or the legal terms are unfavorable. Investors should examine: 🏷️ valuation; 📄 SAFE cap; 💸 conversion discount; 📉 dilution; ⚖️ liquidation preferences; 📌 pro rata rights; 🔒 transfer restrictions; 🧾 information rights; 🌍 jurisdiction; 🧺 capitalization table; 👥 founder ownership; 💼 employee option pool; 🚪 likely exit pathways. Price matters. A good company purchased at an unreasonable price may produce a weak investment return. 16. 💣 Principal risks of venture investing ⚰️ 1. Complete loss A startup can fail, leaving the investor with no recoverable value. For direct early-stage investments, the investor should assume that losing 100% of the amount invested in an individual company is possible. 🔒 2. Long-term illiquidity Venture investments may remain illiquid for: ⏳ 5–10 years Sometimes the period is even longer. There may be no buyer, no public market, and no contractual right to demand repayment. 📉 3. Dilution As the company raises new rounds, an early investor’s percentage ownership may decline. Dilution is not always negative. Owning a smaller percentage of a much more valuable company can still be highly profitable. The problem arises when dilution is severe and the company’s valuation does not grow sufficiently to compensate for it. 🏷️ 4. Valuation risk If an investor enters at an inflated valuation, the startup may need extraordinary growth merely to justify the original price. A later down round , where the company raises money at a lower valuation, may: reduce the value of the earlier investment; create additional dilution; trigger investor-protection provisions; damage employee morale; signal weak demand from new investors. 📄 5. Legal and documentation risk SAFE agreements, convertible notes, shareholder agreements, option plans, and side letters can materially affect investor returns. An investor who does not understand the documentation may discover that: other investors have stronger rights; their ownership is smaller than expected; their shares cannot be transferred; their payout priority is weak; their investment converts under unfavorable terms. 🌍 6. Country and jurisdiction risk Cross-border venture investing can involve: ⚖️ different legal systems; 💵 currency exposure; 🧾 tax-reporting obligations; 🏛️ political risk; 🔒 capital-control restrictions; 📜 export-control requirements; 🛡️ sanctions compliance; 📊 limited access to company information. Ukrainian investors should obtain professional legal and tax advice before investing through a foreign company, fund, syndicate, or special-purpose vehicle. 🧠 7. Psychological risk Venture investing requires patience and emotional discipline. A startup may: remain silent for long periods; miss milestones; pivot to a different product; lose important customers; raise a down round; replace its founders; delay an exit; fail completely. An investor who cannot tolerate uncertainty may make poor decisions, sell at an unfavorable discount, or overconcentrate in apparently “safe” late-stage opportunities. 17. 🛡️ How investors can reduce risk Venture risk cannot be eliminated, but it can be structured and managed. 🧺 1. Build a diversified portfolio Do not invest the entire venture allocation in one company. Diversification across: companies; stages; sectors; geographies; investment years can reduce the impact of an individual failure. However, excessive diversification into weak deals does not create a strong portfolio. Quality and access remain important. 👥 2. Invest with experienced market participants The speakers recommended beginning through communities, investor groups, syndicates, or funds managed by people who have already invested through multiple market cycles. An experienced lead investor may help with: deal sourcing; due diligence; negotiation; documentation; portfolio support; future financing; secondary sales; exit management. Their participation does not guarantee success, but it can reduce avoidable mistakes. 🔍 3. Examine who has already invested The presence of a respected venture fund can be a useful signal. It may indicate that professional due diligence has been completed and that the company has access to a stronger network. However, it is not a guarantee. Professional funds also make unsuccessful investments, and investors should not outsource all judgment to another party’s brand. 💰 4. Look for real commercial evidence Revenue, contracts, retention, and customer usage provide stronger evidence than a presentation alone. The earlier the stage, the less evidence will exist. The investor must then demand a larger potential upside to compensate for the uncertainty. 📄 5. Understand the documents The valuation cap, discount, dilution mechanics, liquidation preferences, and transfer restrictions determine the economics of the investment. These are not administrative details. They directly affect potential returns. 🧠 6. Avoid FOMO Fear of missing out is especially dangerous in venture capital. Statements such as: “Everyone is investing”; “This round closes tomorrow”; “This company will definitely become a unicorn”; “A famous investor has already entered” should never replace due diligence. Urgency may be real, but it may also be a sales tactic. 18. 🏦 Venture investing versus business lending This distinction is particularly relevant for Ukrainian investors familiar with financing small and medium-sized enterprises. 💳 Business lending When an investor makes a loan, the expected return normally consists of: repayment of principal; interest payments; a defined repayment schedule; possibly collateral or guarantees. The lender does not normally participate in unlimited upside if the company becomes extremely successful. The return is contractually limited, but the investor may have stronger repayment rights than an equity holder. 🚀 Venture investing A venture investor shares the company’s business risk. If the startup fails, the investor may lose the entire investment. If the startup becomes very large, the investor may earn substantially more than would have been possible through a fixed-interest loan. 📌 The practical comparison Business lending focuses on: 🛡️ protection; 💵 interest; 📅 repayment; 📊 predictability. Venture capital focuses on: 🚀 growth; ⚠️ risk-sharing; 📈 capital appreciation; 🎯 asymmetric upside. Neither model is universally better. They serve different objectives and require different underwriting skills. 19. 🪖 Defense Tech as a major emerging sector A significant part of the discussion focused on Defense Tech. The sector has expanded because of: the Russian war against Ukraine; other international conflicts; rapid drone development; artificial intelligence; autonomous systems; robotics; computer vision; demand for protection of cities and critical infrastructure. 🔥 When Defense Tech began accelerating The speakers suggested that Defense Tech became significantly more active around: 📅 2023 They also referred to making an initial investment in the sector in: 📅 December 2023 Defense Tech was described as moving from a specialized category toward a mainstream venture sector. 🌍 What is driving interest in Defense Tech? Key factors include: 🪖 modern armed conflict; 🚁 the rapid development of drones; 🧠 AI-enabled targeting and navigation; 🤖 autonomous systems; 🏙️ protection of civilian and industrial facilities; 📡 electronic and economic warfare; 💸 pressure to reduce the cost of military operations; 🛡️ the need to protect personnel. 🤖 A shift from unmanned to autonomous systems Earlier investment theses often focused on unmanned vehicles —platforms that operate without a person physically inside them. Examples include: 🚁 aerial drones; 🤖 unmanned ground vehicles; 🌊 unmanned underwater vehicles. The more recent thesis described in the talk emphasizes autonomy . The objective is to develop systems that can perform missions with little or no continuous human control. This may reduce: operator requirements; personnel risk; communication dependence; training costs; reaction time; operating expenses. 🛠️ Defense Tech categories mentioned in the discussion 🛸 autonomous drones; 🚁 interceptor drones; 🤖 unmanned ground systems; 🌊 underwater vehicles; 👁️ computer-vision systems; 🧠 AI-enabled guidance; 🐝 drone-swarm technologies; 🔫 laser-based defense systems; 📡 microwave systems against drone swarms; 🏙️ systems protecting private and critical infrastructure. 🐝 Drone swarms A drone swarm is a coordinated group of drones that can communicate and act collectively. Instead of operating as isolated devices, swarm participants may: exchange information; divide tasks; adapt to losses; continue a mission if some units are destroyed; coordinate attacks or reconnaissance. This can create substantial military capability, but it also raises serious questions concerning safety, accountability, communications resilience, and control over autonomous lethal systems. ⏱️ A very short technology cycle The speakers referred to a battlefield innovation cycle of approximately: ⏱️ 45 days The meaning was that technologies and countermeasures can change so quickly that a product may need significant adaptation within a very short period. They also stated that products may need to be revised approximately every quarter. For an investor, this creates both opportunity and risk. A company can grow rapidly if it solves an urgent problem. However, its technology may also become obsolete quickly if it cannot adapt. 20. 📊 Important figures from the talk in one place 🏢 Startup Network, Network VC, and Unicorn Events 📌 Startup Network was launched in the United States in 2015 . 📌 The platform was described as containing approximately 150,000 startups . 📌 Those startups were said to represent 125 countries . 📌 Unicorn Events was described as operating for approximately 15–16 years . 📌 Approximately 400 events had been organized. 📌 Activities were said to cover approximately 55 countries . 📌 Startups associated with the ecosystem were said to have raised more than $1 billion . 📌 The portfolio discussed contained approximately 110 startups . 📌 Some portfolio companies were described as producing or indicating approximately 30x and 50x outcomes. 🌍 Global unicorn market 📌 A startup valued above $1 billion is called a unicorn. 📌 The combined valuation of unicorn companies was described as approximately $8.6 trillion . 📌 Approximately 50% of unicorns were said to be located in the United States. 📌 Approximately 20% were said to be located in China. 📌 Approximately 5% were said to be located in India. 📌 Approximately 5% were said to be located in the United Kingdom. 📌 Together, these four countries were said to represent approximately 80% of global unicorns. 🪜 Financing stages 📌 A Silicon Valley pre-seed round was described as reaching up to approximately $500,000 . 📌 Y Combinator’s early-stage investment was described as approximately $500,000 . 📌 A seed-stage valuation was described as reaching approximately $20 million . 📌 An average seed raise was described as approximately $3.5 million . 📌 Example seed rounds included approximately $1.5 million , $3.5 million , and $5 million . 📌 An indicative Series A raise was described as approximately $15 million . 📌 Venture-fund checks of $5 million , $10 million , $20 million , and sometimes $100 million were mentioned. 📌 Private-equity funds may invest amounts measured in hundreds of millions or billions. 💸 Risk and startup mortality 📌 Out of 1,000 startups , approximately 10 were said to have the potential to become unicorns. 📌 A very early-stage startup was associated with an illustrative failure probability of approximately 55% . 📌 After approximately $2 million had been invested, the failure probability was described as falling to approximately 14% . 📌 One specific portfolio was said to have experienced approximately 10% startup mortality at that point, although the speakers acknowledged that general market mortality is higher. 🚪 Exits 📌 Startups almost never pay dividends. 📌 Approximately 90% of exits were described as occurring through M&A. 📌 Approximately 10% were described as occurring through IPOs. 📌 Secondary sales can allow investors to sell some shares before an IPO or acquisition. 📄 Investment instruments 📌 Historically, convertible notes were described as approximately 90% of early-stage instruments and SAFEs approximately 10% . 📌 The speakers stated that the proportions have now largely reversed. 📌 Approximately 40 criteria were said to be used in startup evaluation. 📈 Revenue and traction 📌 More than $1 million in revenue was mentioned as an important threshold for certain syndicated deals. 📌 Examples of companies with approximately $8 million and $10 million in revenue were mentioned. 📌 Strong annual revenue growth was discussed in the context of approximately 3x per year . 📌 One startup was described as increasing sales by 10 times in one year . 📌 Another example had grown to tens of millions of dollars in sales . 🪖 Defense Tech 📌 Defense Tech was described as accelerating from approximately 2023 . 📌 The first referenced investment in the sector was made in December 2023 . 📌 The battlefield technology cycle was described as approximately 45 days . 📌 Products may require adaptation approximately every quarter. 🔒 Private-company secondary transactions 📌 Private shares may be sold at significant discounts because of lock-ups and transfer restrictions. 📌 A discount of approximately 70% was discussed in one example. 21. 🧭 How a Ukrainian investor can begin Step 1. 📚 Learn before investing The first step should not be transferring money. The investor should first understand: what a SAFE is; what a valuation cap is; how a conversion discount works; how dilution works; how to read a capitalization table; how startup rounds are structured; how exits occur; how syndicates operate; how venture funds build portfolios. Education does not remove risk, but it reduces avoidable errors. Step 2. 💸 Define a limited venture allocation Venture capital should normally represent only the part of an investor’s capital that can remain illiquid and can potentially be lost. An investor should not use: emergency savings; money needed for near-term expenses; borrowed money; capital required to support the investor’s primary business; funds that must remain liquid. Step 3. 🧺 Avoid relying on one startup Portfolio construction is central to venture investing. One startup is a highly concentrated speculation. Ten companies may offer better diversification. Twenty or more may provide more opportunities to capture an outlier. However, the appropriate number depends on: the investor’s capital; minimum check sizes; access to deal flow; follow-on reserves; sector concentration; investment strategy. Investing through a fund may provide diversification more efficiently than building a direct portfolio. Step 4. 👥 Start through experienced investors A beginner may find it safer and more educational to participate through: an investor club; a syndicate; a venture fund; a professional community; a reputable platform with curated deal flow. The quality of the lead investor, fund manager, or platform should itself be carefully evaluated. Step 5. 🔍 Analyze each opportunity Before investing, determine: Who are the founders? What problem is being solved? How large is the market? Does the company have a product? Does it have revenue? How quickly is it growing? Who are the competitors? Who has already invested? What is the valuation? What are the SAFE or equity terms? How could an exit occur? What could cause the company to fail? 22. ✅ Checklist before a first venture investment Before investing, ask: ✅ Do I understand that I could lose the entire amount? ✅ Is this only a limited part of my overall investment portfolio? ✅ Do I know the startup’s financing stage? ✅ Does the company have a functioning product? ✅ Does it have revenue or meaningful traction? ✅ Is the target market large enough? ✅ Is the founding team credible and capable? ✅ Does the company have a genuine competitive advantage? ✅ Do I understand the valuation? ✅ Have I read the SAFE, note, or shareholder documents? ✅ Do I understand the cap, discount, and dilution? ✅ Do I know who else has invested? ✅ Is there a credible path to an exit? ✅ Is this investment part of a diversified strategy? ✅ Can I leave the money invested for 5–10 years? ✅ Am I acting based on analysis rather than FOMO? If the answer to most of these questions is no, the investor should continue learning before committing capital. 23. 🚫 Common beginner mistakes ❌ Investing all available capital in one startup. ❌ Investing only because the idea sounds exciting. ❌ Ignoring legal documents. ❌ Failing to understand dilution. ❌ Treating a private valuation as immediately realizable cash. ❌ Expecting dividends. ❌ Assuming an IPO will happen quickly. ❌ Investing without understanding the exit mechanism. ❌ Following market hype. ❌ Copying a famous investor without independent analysis. ❌ Failing to reserve capital for future rounds. ❌ Investing money that cannot be lost. 24. 🧠 What it means to become a venture investor Becoming a venture investor means more than buying an interest in a startup. It requires accepting a different investment model. A venture investor understands that: some startups will fail; some will survive without generating meaningful returns; one or two companies may create most of the portfolio’s value; dividends are highly unlikely; capital may remain locked for years; legal terms materially affect returns; a valuation is not the same as cash; an exit may never happen; access to high-quality deal flow is critical; portfolio construction matters more than one attractive deal. Direct venture investing is not fully passive. It requires: 📚 continuous learning; 🔍 due diligence; 🧠 judgment; 🤝 access to professional networks; ⏳ patience; ⚠️ tolerance for uncertainty. 25. 🏁 Conclusion Venture capital is one of the most attractive and one of the riskiest forms of investing. It is not designed to preserve capital. It is not suitable for investors who require guaranteed returns. It is not suitable for investors who need immediate liquidity. It may be appropriate for investors who: 🚀 want exposure to technological growth; 🧠 are prepared to study the market; 🧺 understand portfolio construction; 💰 can risk a limited part of their capital; 🌍 want exposure to global startup ecosystems; 🤖 are interested in AI, Defense Tech, software, robotics, autonomous systems, and other emerging technology cycles. The basic formula is: 🧠 Knowledge + diversification + access to strong deals + patience + risk tolerance A successful venture investor does not succeed by eliminating risk. The investor succeeds by understanding risk, pricing it, structuring it, diversifying it, and maintaining enough exposure to benefit when an exceptional company emerges. ⚠️ Important disclaimer This article is educational and is based primarily on statements made during the referenced talk. The market figures, failure probabilities, geographic percentages, round sizes, and exit distributions were presented by the speakers and have not been independently verified in this article. They should not be interpreted as: financial advice; a guarantee of returns; a recommendation to invest in a particular startup, fund, or platform; a substitute for legal, tax, or financial due diligence. Venture investments may result in the complete loss of invested capital. Ukrainian investors considering cross-border transactions should consult qualified legal, tax, and investment professionals.

Review and newsAIReviewsBefore investing

🚀 SpaceX IPO: A Big Opportunity or a Hype Trap for Investors?

SpaceX is going public. And this time, according to the information provided, it is no longer just a rumor. The company officially launched its IPO roadshow on June 4, 2026 . It plans to sell 555,555,555 Class A shares at an expected price of $135 per share and wants to trade on Nasdaq under the ticker SPCX . This sounds like a historic event. And in many ways, it is. SpaceX means rockets, Starlink, satellites, Starship, AI infrastructure, and Elon Musk. But for investors, the most important question is not whether SpaceX is famous. It is not even whether SpaceX is an important company. The real question is much simpler: Are investors paying too much for the dream? 💸 📌 What is actually happening? An IPO is when a private company sells shares to public investors for the first time. Before an IPO, regular investors usually have very limited access to a company like SpaceX. After the IPO, shares can be bought through a broker, such as Interactive Brokers, assuming the investor has access to U.S. stocks. SpaceX plans to list on the Nasdaq Global Select Market and Nasdaq Texas under the ticker SPCX . The expected IPO price is $135 per share . At that price, SpaceX could raise around $75 billion . If underwriters use the additional option to sell another 83,333,333 shares , the company could raise around $86.25 billion . The implied market value would be around $1.765–$1.776 trillion . That is enormous. In simple words, investors would not only be buying SpaceX as it exists today. They would also be paying for a very big future story. 🧩 What are investors really buying? SpaceX is not just a rocket company. It is several major investment stories inside one company. 1. 🚀 The launch business SpaceX has become one of the most important companies in orbital launches. Based on the information provided, since 2023 it has delivered more than 80% of the world’s mass to orbit , completed around 650 launches , and built a strong advantage through rocket reuse. This is a powerful business. SpaceX has changed the economics of space launches. But it is also expensive. Rockets, launch sites, vehicles, testing, infrastructure, and engineering all require huge amounts of capital. 2. 📡 Starlink: the key financial engine Starlink is SpaceX’s satellite internet business. Right now, it appears to be the most financially important part of the company. According to the provided information, SpaceX’s Connectivity revenue, which includes Starlink, grew from: $3.9 billion in 2023 to $7.6 billion in 2024 to $11.4 billion in 2025 . Connectivity adjusted EBITDA also grew from: $1.6 billion in 2023 to $3.8 billion in 2024 to $7.2 billion in 2025 . In simple terms, Starlink is no longer just an exciting idea. It is already a large business with millions of customers. SpaceX also says Starlink reached 10 million active customers . 3. 🤖 The AI story: exciting, but risky SpaceX is also including an AI-related story in its IPO materials. This matters because AI is one of the biggest themes in the stock market. But there is an important warning sign. According to the provided information, SpaceX’s AI revenue was: $3.0 billion in 2023 $2.6 billion in 2024 $3.2 billion in 2025 . These are large numbers. But AI adjusted EBITDA reached negative $1.2 billion in 2025 . In simple words: the AI business is producing revenue, but it is still burning a lot of cash. According to the provided information, only the Connectivity business is currently profitable, while the space and AI segments are still using cash. 💰 The biggest issue is not the company. It is the price. SpaceX is an extraordinary company. That is not the main debate. The problem is valuation. A great company is not always a great investment if the entry price is too high. According to the information provided, SpaceX had $18.67 billion in revenue in 2025 and a net loss of $4.94 billion . At a valuation of around $1.75 trillion , that is about 94 times annual revenue . For a regular investor, this means the market is already pricing SpaceX as if many things go right: Starlink keeps growing. Starship becomes commercially successful. The AI business becomes real and profitable. SpaceX keeps its lead in launches. Investors remain comfortable with Elon Musk’s control. That is a lot of future success already included in the price. According to the information provided, Morningstar reportedly valued SpaceX at around $780 billion , which is less than half of the IPO target valuation. Some investors reportedly wanted a valuation closer to $1.5 trillion or lower. So the key question is not: “Is SpaceX a great company?” The real question is: “At what price does even a great company become too expensive?” ⚖️ 📈 How can a regular investor make money? There are two main ways. ✅ Option 1. Get shares at the IPO price This is the most attractive route. For example, an investor receives shares at the IPO price of $135 before trading begins. If the stock opens at $180 , the paper profit is $45 per share . Simple example: An investor buys 20 shares at $135 . Total investment: $2,700 . If the investor sells at $180 , the total sale value is $3,600 . Gross profit: $900 , before taxes, FX costs, and fees. But there is one big problem: IPO allocation is not guaranteed. An investor may request 20, 50, or 100 shares and receive fewer shares — or zero. Through Interactive Brokers, some IPOs may be available through Client Portal → Trade → IPO Subscriptions . But access depends on the investor’s country, account type, regulation, and the specific offering. For Ukraine-based investors, the key practical question is simple: does this IPO subscription appear inside your own IBKR account? If it does not appear, the more realistic route may be buying SPCX after trading begins. ⚠️ Option 2. Buy SPCX after trading begins This is easier, but riskier. Once SPCX starts trading on Nasdaq, investors with access to U.S. stocks may be able to buy it like any other public U.S. stock. But the danger is the opening price. If the IPO price is $135 , but the stock opens at $200 , then the investor is not buying “the IPO at $135”. They are buying a much more expensive stock. Here is the risk: The investor who received shares at $135 may still be profitable even if the stock later falls to $150 . But the investor who bought at $200 would be down 25% if the stock falls to $150 . That is why market orders can be dangerous during the first minutes of a hot IPO. A market order can execute at a much higher price than expected. A more disciplined approach is a limit order . This means the investor sets the maximum price they are ready to pay. For example: “I am willing to buy SPCX only at $170 or lower .” This does not guarantee a purchase. But it protects the investor from buying at a price that is too high. 🧠 What do recent big IPOs teach us? Recent IPO history shows that the first day can be very profitable. But it can also be dangerous for investors who buy too late. Arm priced at $51 and closed its first day at $63.59 , up about 25% . Reddit priced at $34 and closed its first day at $50.44 , up about 48% . Airbnb priced at $68 and closed its first day at $144.71 , more than doubling. Snowflake priced at $120 and closed its first day at $253.93 , also more than doubling. But there are also warning examples. Rivian priced at $78 , closed its first day near $100.73 , and later traded much lower, around $18.12 . Coinbase, which went public through a direct listing, closed its first day at $328.28 and later traded around $164.13 . The lesson is very clear: Getting shares at the IPO price and buying after a huge first-day jump are two completely different trades. 🔮 Three possible scenarios for SPCX 🟢 Scenario 1. Strong first-day jump This is very possible. SpaceX has a powerful brand. It has Elon Musk. It has Starlink. It has the space story. It has the AI story. And many investors may want exposure to the company. If the stock jumps 20–50% on the first day, that would not be surprising for such a high-demand IPO. At an IPO price of $135 : a 20% jump means around $162 per share ; a 50% jump means around $202.50 per share . But the higher the stock price goes, the more expensive the company becomes. At those levels, SpaceX’s valuation could move from around $1.75 trillion to around $2.1–$2.6 trillion . That makes the valuation even more demanding. 🟡 Scenario 2. Huge first-day jump, then volatility Airbnb and Snowflake showed that very hot IPOs can double on the first day. If SpaceX doubled from $135 to $270 , the company’s valuation could move toward $3.5 trillion . That would place SpaceX near the largest public technology companies in the world. This could happen because of demand, hype, and limited available shares. But fundamentally, investors would need to believe that Starlink, launches, Starship, AI compute, and future orbital infrastructure can justify one of the highest valuations in the public market. 🔴 Scenario 3. The hype fades This is the risk many retail investors underestimate. A stock can open strongly and still fall later. Investors may start focusing on the company’s $4.94 billion net loss , heavy AI spending, Starship execution risk, regulation, competition, and corporate governance. A 20–40% decline from a hot first-day trading price would not be impossible. In many hyped IPOs, the better buying opportunity appears weeks or months later — after the first wave of excitement cools down. 📊 Why Nasdaq-100 matters There is one bullish factor: possible index demand. According to the provided information, Nasdaq updated its Nasdaq-100 rules in 2026 and created a faster path for some of the largest new listings. A new listing can be evaluated after its seventh trading day if it ranks in the top 40 by full market capitalization. This matters because if SpaceX enters the Nasdaq-100 quickly, funds tracking Nasdaq-100 products may need to buy SPCX shares. That could create additional demand. But the S&P 500 is different. According to the provided information, IPOs still need to trade on an eligible exchange for at least 12 months before they can become eligible for S&P 500 inclusion. So the simple version is: Nasdaq-100 could become a near-term catalyst. S&P 500 is not an immediate catalyst. 👤 Elon Musk’s control: what it means for investors After the IPO, Elon Musk is expected to keep around 84.4% combined voting power . For regular investors, this means they may own shares, but they will not control the company. SpaceX is also expected to be a controlled company under Nasdaq rules. This may allow it to use certain corporate governance exemptions. In simple words: You can buy the stock. But Elon Musk and key shareholders will still control the direction of the company. 🔒 Lock-up risk: the first trading day is not the whole story There is also lock-up risk. A lock-up is a period when insiders and major shareholders cannot sell shares after the IPO. According to the provided information, Elon Musk has a 366-day lock-up , while other investors, officers, directors, and shareholders have staggered lock-up schedules. Why does this matter? When lock-ups expire, more shares may become available for sale. Even the expectation of future selling can put pressure on the stock price. So investors should not judge the whole opportunity only by the first day of trading. Important supply events can happen later. 🧭 Final view for regular investors SpaceX IPO could be one of the biggest listings of 2026. The company has a powerful brand, a real and growing Starlink business, a dominant launch position, and a very ambitious story around AI and future infrastructure. But the risk is also high. At a valuation of around $1.75 trillion , SpaceX is already priced as if many things go right. Starlink must keep growing. Starship must become economically successful. The AI business must improve. Investors must stay comfortable with Elon Musk’s control. The best risk/reward is likely for investors who receive shares at the IPO price of $135 . The riskiest entry is buying blindly after a huge first-day jump. The main rule is simple: Do not chase the rocket if it has already flown too high. 🚀 SpaceX may become a major public investment story. But even the best company can become a bad investment if bought at the wrong price. 🇺🇦 Possible impact on Ukrainian investors, business, and the investment market 1. 📈 More Ukrainian investors may become interested in IPOs If SpaceX IPO becomes a major global event, more Ukrainian investors may start learning about U.S. IPOs, Nasdaq, Interactive Brokers, ETFs, and global tech stocks. This could improve financial education. But it could also increase emotional buying if people invest only because “everyone is talking about SpaceX.” 2. 💸 Some capital may move from local investments to global stocks A hot SPCX listing could pull attention and money away from Ukrainian investment opportunities, including local businesses, startups, real estate, and bonds. That may be negative for the local investment ecosystem if too much private capital flows into foreign hype-driven assets. 3. 🛰️ Ukrainian defense-tech, AI, and infrastructure startups may benefit from the narrative SpaceX IPO could remind investors that space infrastructure, satellite connectivity, AI infrastructure, and defense-related technologies are huge markets. This is important for Ukraine because the country already has strong engineering teams, AI developers, drone companies, defense-tech startups, and communications-focused solutions. 4. ⚠️ Retail losses could damage trust in investing If many retail investors buy SPCX too high and then face a sharp correction, some may conclude that “the stock market is a casino.” That would be harmful for Ukraine’s investment culture. This is why education matters: investors need to understand valuation, limit orders, risk size, diversification, and entry price. 5. 🚀 The biggest lesson for Ukrainian business SpaceX is not just selling rockets. It is selling a future infrastructure platform. For Ukrainian founders and businesses, the lesson is clear: investors pay premium valuations for companies that combine technology, infrastructure, brand, scale, and a big market vision. The challenge for Ukraine is to build more companies that can tell that kind of story — but with real numbers behind it.

Review and newsFood serviceReviewsBefore investing

What Is Happening to Ukraine’s Restaurant Market: A Founder’s View from Molodist and Kyiv Food Market