What’s going on?

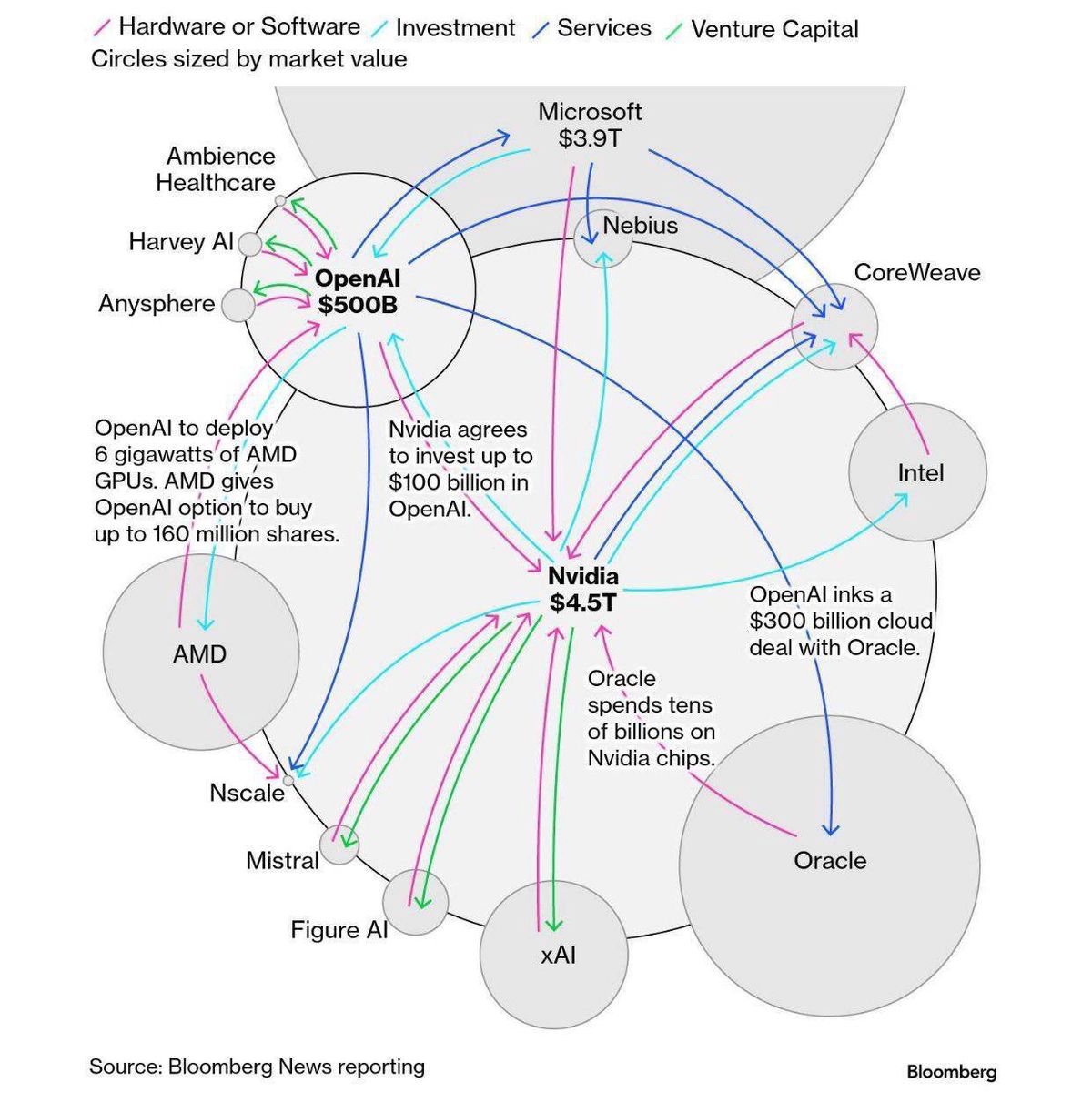

A Bloomberg chart maps how AI’s biggest players simultaneously buy from, sell to, and invest in each other. The loop looks like this:

— multi-year cloud deals;

— tens of billions spent on GPUs;

— cross-investments and options that inflate paper valuations.

Shown on the graphic: Nvidia (about $4.5 trillion), Microsoft (about $3.9 trillion), OpenAI (about $500 billion valuation), plus Oracle, AMD, Intel, CoreWeave, xAI, Mistral, Figure AI, and more. Examples on the chart include OpenAI’s hundreds-of-billions cloud deal with Oracle, Oracle spending tens of billions on Nvidia chips, Nvidia agreeing to invest up to $100 billion into OpenAI, and OpenAI deploying 6 gigawatts of AMD GPU power with an option to buy up to 160 million AMD shares.

Why this can inflate valuations

Vendor financing: suppliers invest in customers to secure future demand.

Long-dated contracts: huge take-or-pay-like commitments create an aura of guaranteed growth.

Equity and options: cross-stakes lift marks without proven cash returns.

Profits tomorrow: capex today, hoped-for monetization tomorrow.

Similarities and differences vs. 2007

Yes, there are tangible assets this time (chips, data centers, electricity). But hidden risks remain: vendor concentration, off-balance cloud commitments, dependence on cheap power, and regulatory pushback. If AI revenue lags capex, marks can be revised — sharply.

Key risks to watch

— Concentration in a single supplier (Nvidia);

— Monetization gap between AI usage and actual revenue;

— Power and cooling constraints (gigawatt-scale projects);

— Private-market liquidity (secondary sales at discounts).

What to track in disclosures

— Cost per 1k tokens or per inference vs. price charged;

— Gross margin of AI features;

— Data-center utilization;

— Capex per dollar of revenue;

— The project’s power mix and cost.

Implications for Ukraine

Opportunities in ML engineering, MLOps, defense-tech AI, inference optimization, and energy-efficient data-center tooling. Be cautious with “GPU farms without customers”, vendor-financed loops, and lofty multiples unsupported by cash flow. Potential alpha: power management, cooling, inference efficiency, vertical AI with clear ROI in healthcare, agri, logistics, and security.

Bottom line

This is a massive bet on fast AI monetization. If revenue catches up with capex — everyone wins. If not, a painful re-rating comes.

Scenarios for Ukraine’s investment market

— 🟢 Soft cool-down: valuations compress but infra stays busy; steady demand for Ukrainian engineering and defense-tech AI.

— 🟠 ROI reset: enterprises trim AI budgets; down-rounds; cheaper “iron” locally but stronger demand for ROI-first solutions.

— 🔵 Supercycle: productivity boom proves out; FDI into near-EU data centers and acquisitions of Ukrainian AI products.

Source: Bloomberg News reporting graphic. Not investment advice.