1. What Happened? 🤔

GDP +5.4 % in Q1 2025, yet tax revenue –3.5 % (-¥174 bn / –$23.8 bn).

Land-sale income –40 %, gutting local budgets.

Provincial debt above ¥100 trn; wage cuts and delays hit civil servants.

Export “front-loading” before April US tariffs padded GDP but not taxable profits.

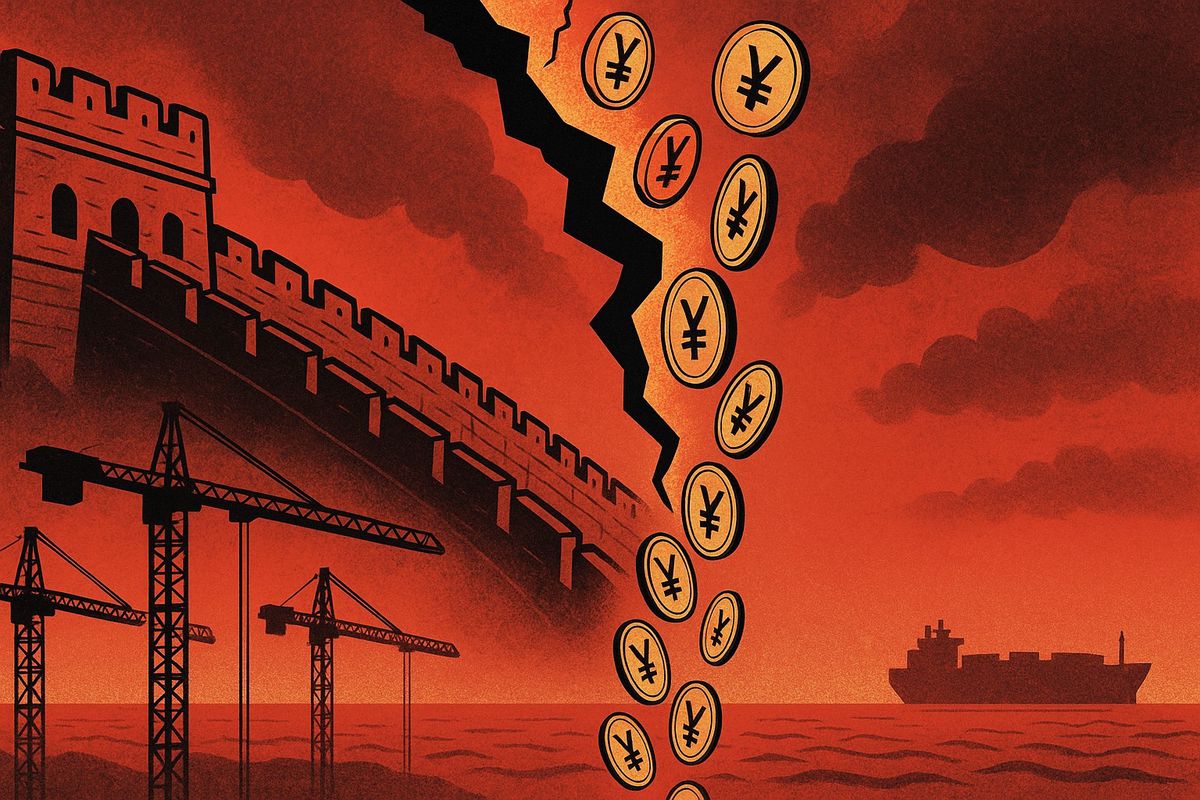

2. Root Causes 🌱

1994 tax split: Beijing kept ~55 % of revenue, provinces stuck with 70 % of spending.

Land-sale addiction crowded out real taxation.

Property bust (2021-25) erased developers and cash flow.

Deflation & weak demand = thinner VAT/ profit margins.

Tax raids squeeze SMEs and chill growth.

3. Global Ripples 🌊

Supply-chain shocks raise costs for electronics, autos.

Commodity chill: softer demand for steel, copper, oil.

Investment re-routing toward Southeast Asia and Eastern Europe.

4. Implications for Ukraine 🇺🇦

Opportunity Track – Capital fleeing China may scout transparent Ukrainian tech & agro plays; cheaper Chinese machinery lowers capex.

Downside Track – Global slowdown could depress metal & grain prices and lift funding costs.

Balanced Track – New manufacturing niches open, but volatility persists; focus on value-added production and diversified exports.

Key Takeaways

China faces its toughest fiscal hole since the 1990s reforms.

Land sales proved a sandy foundation for local budgets.

Ukrainian investors must hedge globally yet court funds seeking safer emerging markets.